Flex seat transactions up 2.5X Y-on -Year for FY 2021-22 says a report by international property firm JLL and Qdesq.

By Varun Singh

Demand for flex continues to surge as workplace transformation and portfolio strategies make a case for a more flexible, agile, and modern workspace.

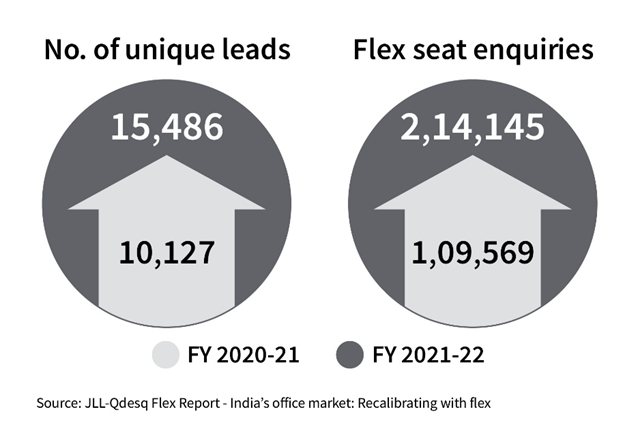

As per a joint report by Qdesq and JLL titled Indian Office market: Recalibrating with Flex the aggregate enquiries for flex space witnessed nearly a 2X Y-o-Y growth for FY 2021-22. This translated to over 214,000 flex seats spread over 15,000 unique leads as recorded by Qdesq across the major Tier I and II cities. In terms of space, with 1 flex seat = 70 sq. ft of leasable area on an average, this translates to nearly 15 million sq ft.

- Enquiries for flex seats record a 95% growth in the same period

- 90,200 + flex seats were transacted in FY 2021-22 in the top seven cities

- Tier 1 cities account for 78% of total flex space

- Delhi NCR, Bengaluru, Chennai, and Mumbai, together with lead in seat enquiries

- Number of unique leads, represented by entities either corporates or individuals, has grown by 53% year-on-year (Y-o-Y) across leading Tier I & II cities

Qdesq tracks the unique leads and flex seat enquiries on its digital and offline platform. JLL

tracks the actual flex seat transitions. Therefore, the data has been drawn after benchmarking leads and enquiries against actual transactions. Also, interesting to note

is that the average deal size (number of seat enquiries/number of leads) has increased by

around 27% – from an average of 11 seats in FY 2020-21 to an average of 14 seats in FY 2021-22.

According to JLL 90,200 + flex seats were leased across the top 7 cities by occupiers in FY 2021-22 which is a 2.5X growth Y-o-Y. This shows that demand for flex space has seen a significant resurgence over the past 12 months, driven by enterprises seeking to create a more agile real estate portfolio strategy in an evolving hybrid work environment.

62% of the seats transacted were taken up through the managed route, where the flex operator was curating the entire flex workspace as per the tenant’s needs. This outlines how flex is transforming as per the needs of the market from a pure coworking set-up to a more private office, managed space concept. This is reiterated further with seat enquiries showing a higher demand for private offices (43%) compared to coworking set-ups (39%).

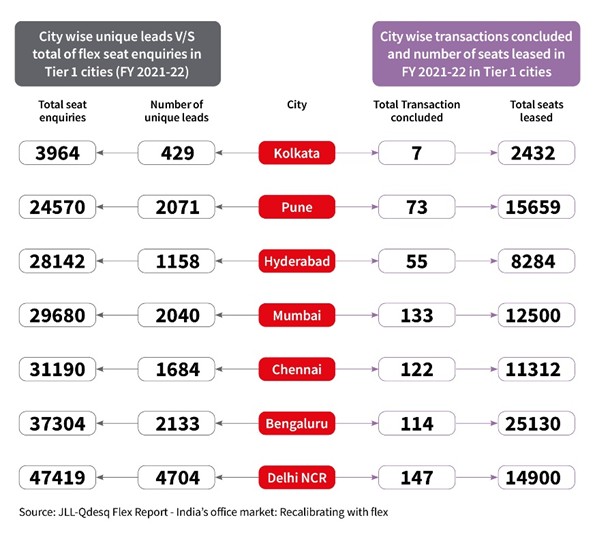

Delhi NCR, Bengaluru, Chennai, and Mumbai, together with lead seat enquiries

Delhi NCR leads in terms of unique leads and total seat enquiries. In fact, the top four cities in terms of seat enquiries – Delhi NCR, Bengaluru, Chennai, and Mumbai, together account for about 74% of the leads and 72% of the seat enquiries, respectively. Bengaluru is the leading tech hub and along with Delhi-NCR forms the two major start-up clusters in the country and thus sees a significant demand also coming from big tech firms and well-funded unicorns

Flex seat enquiries up 17% Y-o-Y in Tier-II cities

Start-ups, SMEs, and companies in the fintech and e-commerce segments focusing on emerging economic centres and smaller towns for business growth and enterprises looking to tap into the talent pool of an increasingly mobile workforce are the mainstays of this rise in enquiries for flex seats in Tier-II cities as per the report.

Chandigarh, Indore, and Lucknow are seeing robust traction for flex enquiries. In fact, there is good traction across major Tier-II cities in the North, West, and South.

Bengaluru, Pune, and Delhi NCR together account for over 60% of the total flex seats leased in FY 2021-22 More than half of the total flex seats leased in FY 2021- 22 were in the form of significant-sized transactions of 300 or more seats. In absolute terms, Bengaluru saw around 25,000 flex seats leased, followed by Pune with around 15,000 over the same 12-month period. “The flexibility to expand or contract on-demand, shorter lease tenures, fully serviced, amenity-rich offices and being able to create workspaces of the future which act as magnets for returning employees and in the war for talent are key factors fueling the flex market growth. An increasing number of enterprises are expanding their usage of flex space in tandem with transformational changes with respect to remote work, mobility, and flexibility. We expect the flex footprint to grow to nearly 75 million sq. ft by 2025 from the current 40 million sq ft levels, riding the wave of enterprise demand for managed workspaces.” said Dr Samantak Das, Chief Economist and Head of Research and REIS, India, JLL.

MSMEs & Others’ category drive aggregate enquiries, but enterprises from tech and start-up ecosystems driving actual seat take-up

As per the JLL-Qdesq report, aggregate enquiries are driven by ‘MSMEs & Others’ category across non-tech industries followed by tech and startups. These three segments together account for 59% of the flex space enquiries. JLL’s data on actual flex seat transactions shows that enterprises across a wide spectrum but led by tech and startups are now driving conversations around demand for flex and even actual space take-up. Tech and start-ups together contribute 48% of the actual flex space take-up.

“Flex industry has grown drastically in popularity and adoption among Indian corporates of all sizes & scale, over the last few years. All forms of Flex – Coworking, Private managed office, and Hybrid on demand usage, are experiencing robust demand. Having said that, Coworking stands out as the best fit and solution for sub 100 seats requirement which is 90% of the market. Enterprises have been re-evaluating the office strategy and return to work equations. All the cues leading to a phenomenon of employee-centric and productivity-driven office strategy. Furthermore, the things which are constantly being validated are “Flexibility, agility & Decentralisation,” said Paras Arora, Founder & CEO of Qdesq.

We do expect that key groups constituting a fair share of the aggregate enquiries like education and fintech will feature more prominently in the seat take-up pie going forward as these emerging segments make a move from late stages of remote working to a more physical workplace environment.