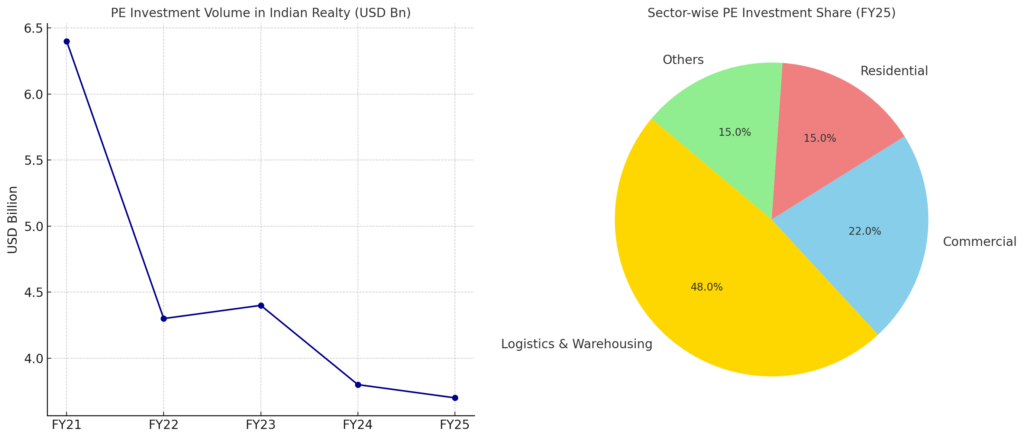

Private equity (PE) investments in Indian real estate have continued their downward trend in FY25, falling to USD 3.7 billion, a 43% drop from FY21’s peak of USD 6.4 billion. However, a new report by ANAROCK Capital reveals a shifting strategy among investors: fewer deals, but much larger in size, signaling increased focus on high-value, stable opportunities.

According to the FLUX FY25 Annual Edition, only 39 PE deals were recorded this fiscal—down from 51 in FY24—but the average deal size jumped to USD 94 million, up from USD 75 million last year.

“The market is evolving,” said Shobhit Agarwal, MD & CEO, ANAROCK Capital. “Capital is consolidating around fewer, better-quality assets, and that’s a sign of maturity in the investment landscape.”

Top Deals Highlight New Investment Focus

Some of FY25’s biggest deals include:

- GIC-Xander → Shapoorji Pallonji – USD 258 Mn

- Keppel Land → RMZ Corporation & CPPIB – USD 251 Mn

- Blackstone → LOGOS India & Kolte Patil – USD 338 Mn combined

- Alpha Wave Global → Oberoi Realty – USD 145 Mn

These top 10 deals alone made up 81% of total PE investment, with the Reliance–ADIA–KKR hybrid transaction contributing nearly half of that.

Foreign Investors Back in the Game

Foreign capital played a dominant role this year, contributing 84% of total investments, up from 68% in FY24. This USD 3.1 billion influx signals renewed global confidence in India’s real estate fundamentals, despite international economic volatility.

Warehousing Emerges as Sector Champion

For the first time in five years, logistics and warehousing captured 48% of total PE funding, emerging as the most preferred sector. This shift reflects rising demand from e-commerce, manufacturing, and 3PL players, alongside investor appetite for Grade A, ESG-compliant assets.

In contrast, commercial office investments fell sharply to USD 806 million (from USD 2.2 billion in FY24), as investors remain cautious due to interest rate pressures and geopolitical uncertainty.

Pan-India Plays and Hybrid Deals on the Rise

Multi-city and pan-India transactions accounted for 52% of all investments, up from just 25% in FY23. Investors are increasingly opting for diversified portfolios that spread risk and maximize returns across locations.

Also notable is the rise in hybrid deal structures, which made up 42% of total funding, a major shift from previous years where equity dominated. Pure equity and debt fell to 37% and 21% respectively.

“The rise of hybrid structures reflects more creative, tailored investment strategies,” said Aashiesh Agarwaal, SVP & Investment Advisor at ANAROCK Capital.

Sector Snapshot

- Residential: Entering consolidation, though foreign players like Blackstone and Alpha Wave are showing interest.

- Retail: Growing via REITs and large players like DLF and Phoenix; PE activity remains subdued.

- Commercial: Leasing stays strong, but capital flow is cautious amid high borrowing costs.

- Logistics & Warehousing: Strong long-term outlook with structural demand drivers in place.

Outlook: Strategic Growth Ahead

While total investment volumes have dipped, strategic deployment, rising foreign participation, and sectoral realignment are setting the stage for a stronger, more resilient real estate market. ANAROCK’s FLUX FY25 report underscores the need for adaptability in the face of shifting investor priorities and global dynamics.