Institutional investment in 2021 closed at USD 4.3 billion, a decline of 14% over the pandemic year 2020, according to JLL’s ‘Capital Markets Update Q4 2021’

By Varun Singh

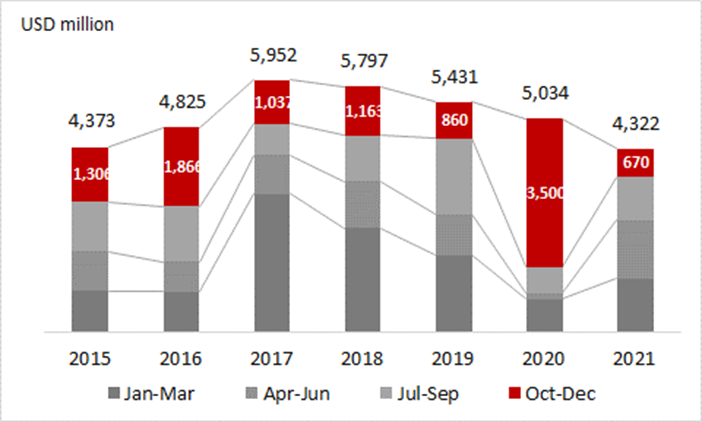

Institutional investment in 2021 closed at USD 4.3 billion, a decline of 14% over the pandemic year 2020, according to JLL’s ‘Capital Markets Update Q4 2021’ released today. The year 2020 saw a sharp recovery in investments, thanks to two large portfolio deals amounting to USD 3.2 billion announced in the last quarter of the year. On the other hand, investments in 2021 have been much broad-based with the first three quarters reporting improvement as compared to the same quarter the previous year. The year 2021 witnessed 57 deals as compared to 27 deals in 2020. Investment in 2021 were spread across various sectors and were much more diversified as compared to the previous year. The onset of the third wave led to overall restrictions which indirectly impacted the investment momentum during the last quarter of the year.

“One of the major reasons for the decline in investment volume has been the intermittent breakdown in the investment process due to the severe impact of the second Covid wave during the first half of 2021. Though the investment climate showed signs of recovery during the third quarter of the year, the onset of a new variant and the uncertainty about its impact disrupted deal closures in Q4, 2021. However, beyond the numbers what is important to note is that there is a clear sign of broad-based recovery with positive investor sentiments being seen across all asset classes,” said Lata Pillai, Managing Director and Head, Capital Markets, India, JLL. “I believe our industry is poised for a much stronger 2022 looking at current investment momentum and deal flow that we are seeing on the ground,” she added

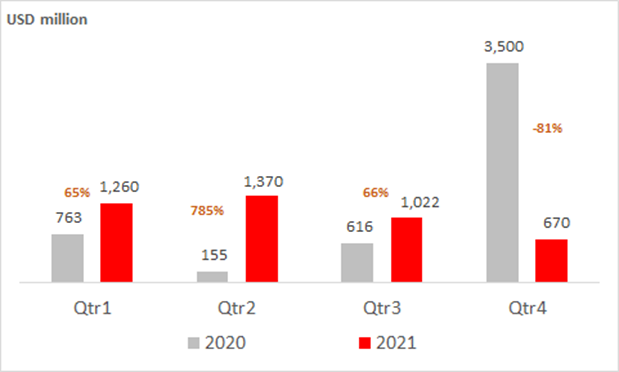

Investment momentum takes a break in Q4 2021

“The comparison of quarterly investment patterns during the last two years indicates that 2021 recorded a smarter recovery as compared to the pandemic year. However, this steam was lost during the last quarter of the year mainly due to the spread of the third wave of the pandemic. The disruption in the investment process, revenue visibility across asset classes, and trends in office space absorption and residential traction dampened the deal flow. As a result, investments during the quarter went into wait-and-watch mode. The overall economic conditions with indications of bottoming out of interest rates and liquidity tapering by the central banks globally also made investors have re-look at their investment strategies. Though the last quarter of the year is the most active period, Q4 of 2021 has been an exception due to the above reasons,” said Dr Samantak Das, Chief Economist and Head of Research & REIS (India), JLL

“However, with improved resilience to uncertainty, investors are expected to keep their investment plans intact. Though the waning of the third wave is a function of societal response and vaccination, other factors supporting growth are still intact. The continued policy support in form of accommodative policy stance, expected push on infrastructure spend and committed dry powder by institutional investors is expected to drive 2022 investments at par with the momentum witnessed during 2017-2020” he added

Office continues to lead at 31%, Residential comes back with 25% share

The year 2021 demonstrated investment diversification across asset classes as compared to being lopsided in 2020. One of the distinguishing features of the investments during the year has been the comeback of the residential sector which has seen the second-highest share of 25%. The residential sector attracted 2.3x investments at USD 1,081 million as compared to USD 460 million in 2020. The renewed interest in the sector has been mainly due to the sharp recovery witnessed with a robust sales growth of 47% during the first nine months of 2021 over the same period of 2020. Investors provided structured funds to the sector as these were closer to the equity returns.

Investments in the office sector accounted for the largest share of 31% during 2021 while it was highly skewed during 2020 due to two large portfolio deals amounting to USD 3.2 billion. Office space net absorption was up marginally by 2% Y-o-Y at 26.2 million sq ft. in the top 7 cities in India as compared to the previous year. Most occupiers have their real estate plans in place and that is likely to result in expected net absorption of 31-33 million sq ft in 2022, up by 20-25% Y-o-Y. Leading office space developers are expected to contribute around 58% of this upcoming supply of 45-47 million sq ft that may open development stage investment opportunities.

Warehousing, logistics, and data centre continue to witness increased interest from investors with logistics accounting for 20% of the total deal volume while data centre investments have started picking up with a few joint ventures announced in the segment.

| Segment | 2020 | % share | 2021 | % share |

| Office | 4,350 | 86% | 1,323 | 31% |

| Residential | 460 | 9% | 1,081 | 25% |

| Warehousing | 94 | 2% | 866 | 20% |

| Retail | – | – | 560 | 13% |

| Alternatives | – | – | 161 | 4% |

| Mixed-use | – | – | 137 | 3% |

| data centres | – | – | 135 | 3% |

| Land | – | – | 60 | 1% |

| Hotels | 130 | 3% | – | – |

| Total | 5,034 | 100% | 4,322 | 100% |

Hyderabad, Mumbai, and NCR account for a 45% share of investments.

Hyderabad and Mumbai each accounted for a 16% share of the total investments during 2021, while NCR-Delhi at 13% stood third. Investments during the year have been quite diversified across cities. On the other hand, consolidation in real estate has led to a parallel trend of increasing investments at the entity level with mergers and acquisitions gaining traction.

| Cities | 2020 (USD mn) | % share | 2021 (USD mn) | % share |

| Hyderabad | 100 | 2% | 687 | 16% |

| MMR | 267 | 5% | 683 | 16% |

| NCR-Delhi | 301 | 6% | 548 | 13% |

| Bengaluru | 3,720 | 74% | 379 | 9% |

| Chennai | 270 | 5% | 150 | 3% |

| Kolkata | – | 0% | 105 | 2% |

| Pune | 61 | 1% | 77 | 2% |

| Other cities | 315 | 6% | 764 | 18% |

| Others* | 0% | 930 | 22% | |

| Total | 5,034 | 100% | 4,322 | 100% |

Hyderabad has been leading the investment scenario with core and development stage transactions by leading global funds. The city has been preferred with marquee office space developers attracting quality tenants at the pre-commitment stage. Office supply in 2022 has already witnessed 25% pre-leasing in select projects and driving the investment momentum. Mumbai has witnessed higher interest in the residential segment due to the sharp recovery in residential home sales during the year.

Outlook

The continued policy support in form of accommodative policy stance, expected push on infrastructure spend and committed dry powder by institutional investors is expected to drive 2022 investments at par with the momentum witnessed during 2017-2020. The build-up of asset portfolios for the listing of new REITs, increased competition for quality assets, geographical and asset diversification and a strong interest for logistics and data centres in the ‘new normal’ will be the major investment drivers during 2022.

Also Read: Now all these details of builders will be available in Public domain