Coworking supply in 2018 was between 7 – 7.5 mn sq. ft. area, this crossed 12 mn sq. ft. by 2019-end

By Varun Singh

The coworking segment continued to grow and established itself as a buzzing real estate segment in 2019. Top 7 coworking players alone have more than 350 centres across India – no. set to double or treble in next 2 years.

“With hip working spaces high on technology, experience and sociability, coworking is no longer just the go-to option for new-age start-ups and entrepreneurs – it has now expanded its reach to mainstream corporates, as well,” says Anuj Puri, Chairman, Anarock Property Consultants.

Major coworking players increased their footprint across the country, institutional funding kept the momentum going. 2019 also witnessed a growing wave of consolidation in the sector, in the form of mergers and acquisitions.

Puri says, “Despite the WeWork debacle in US dominating headlines and raising questions about the future of the coworking business, the segment has emerged as a viable asset class for landlords and operators in India. The coworking market has grown by leaps and bounds and is a significant factor in the strategy for occupiers.”

Millennials & Start-ups to Drive Demand

Millennials are set to form 50% of the global workforce by 2020. This segment has been at the core of the coworking story in India and will continue to drive demand.

India happens to be the world’s youngest start-up nation with >70% founders less than 35 years of age. According to NASSCOM, the end of 2020 will see India have more than 10,500 start-ups, ranking third behind US and UK. As cities like Bengaluru, Gurugram, Pune and Hyderabad witness the rise of the entrepreneurial wave, the demand for coworking spaces is only set to grow in the coming years.

Coworking is no longer driven solely by start-ups, millennials and SMEs – it now caters to mainstream corporates and large enterprises as well (global tech-giant Google leased office space with coworking operator Simpli Work in Gurugram to expand its operations). Even banks and telecom companies are keen on their teams to operate away from headquarters and closer to entrepreneurs.

In 2020, more large companies will opt for flexible coworking spaces for their short-term expansion plans. Supply has been growing with demand – towards 2018-end, the total supply of flexible workspaces was anywhere between 7 – 7.5 mn sq. ft. area – and crossed 12 mn sq. ft. by the end of 2019.

Large Players to Expand Footprint

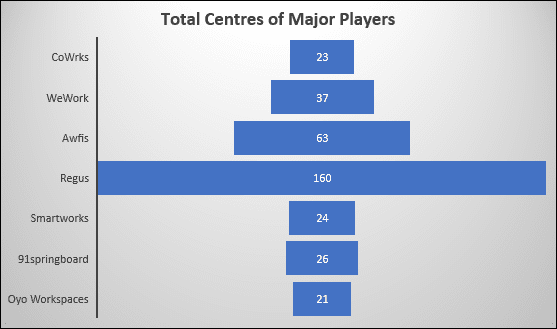

The Indian coworking segment is currently populated by players of varying size and scale. There are currently more than 200 players operating across the country. The top 7 players in this space alone have more than 350 centres across multiple cities in the country. These players include Cowrks, WeWork India, Awfis, Regus, Smartworks, 91springboard and OYO’s Workspaces. This number is likely to double or even treble in the next two years, given the rate at which these leading players actively leased spaces across major cities in 2019.

The coworking sector has also witnessed the entry of major realty players. Bengaluru-based developer Brigade Group ventured into the coworking segment with the launch of ‘BuzzWorks’. Hospitality player Roseate Hotels and Resorts has also forayed into this space by opening its first coworking centre at its hotel ‘Roseate House’ in Delhi’s Aero City.

Even as US-based WeWork’s failed IPO raised doubts about the company’s future, WeWork India’s expansion remained on course. Owned by realty firm Embassy Group, the company has been mainly funded by Embassy so far and pays a management fee to the parent company. With 37 operational coworking centres, the company is currently present in Bengaluru, Mumbai, Gurugram, Pune, Noida and Hyderabad.

Funding Set to Grow

Coworking spaces are fundamentally capital-intensive and revolve around multiple variables such as design, technology, and customer service. For a business that thrives on economies of scale, the backing of institutional capital can be the crucial differentiator. Institutional funding to the coworking space has gradually evolved and grown. While in 2017, most of the deals were driven by angel investors and only a few PE players, 2018 saw the maximum deals driven by large PE players and venture capitalists. This trend continued in 2019, which witnessed strong investor confidence in India’s co-working story with three major deals being inked:

- PE firm ChrysCapital invested USD 30 million in leading player Awfis.

- SmartOwner, a real estate investment fund has put in USD 4.28 mn in Workspace.

- BlackRock & CLSA Capital Partner have invested USD 53 million in GoWork.

PE funds and institutional investors will continue to back bigger players in 2020, allowing them to scale up, expand and offer a standardised experience to customers at more economical prices.

Consolidation

Coworking spaces come in all sizes and variants (even a basement office with about a dozen seats technically qualifies as a coworking space) but not every coworking business is profitable. The success of the business model hinges on the operator’s capacity to scale up, and not every company may have the financial bandwidth or resources to do that. Survival in such a competitive environment will be a challenge for smaller players, and we will see more mergers and acquisitions in 2020.

The consolidation wave had already begunin 2018, with major acquisitions like One Co.Work acquiring IShareSpace and AltF CoWorking acquiring Noida-based Daftar India. The trend continued in 2019 with Oyo taking over Innov8 for INR 220 Cr. In 2020, we will see smaller or city-specific operators merge with national players looking to enter or establish themselves in tier 2 & 3 markets.

Outlook 2020

There’s no doubt that coworking creates an inventive and stimulating work environment, but it also comes with certain risks and conditions. Such a shared format may not be suitable for companies dealing with high volumes of confidential data. It is up to operators to take steps to minimise such risks and scale up cyber security within shared working spaces. The shared work culture also translates into loss of privacy – a major concern for several companies.

To truly realise their potential and grow at a fast clip, coworking players must innovate and re-strategize their business models. The current lease-based structure does not offer much flexibility and cost efficiency. 2020 is likely to see the rise of ownership model developed in partnership with landowners, developers or the space providers. This arrangement will create built-to-suit spaces that are customised as per the tenant’s needs.

There’s no doubt about the scope of coworking sector and its potential for growth in India, but it will take a few more years for co-working to become India’s most-preferred work ecosystem.