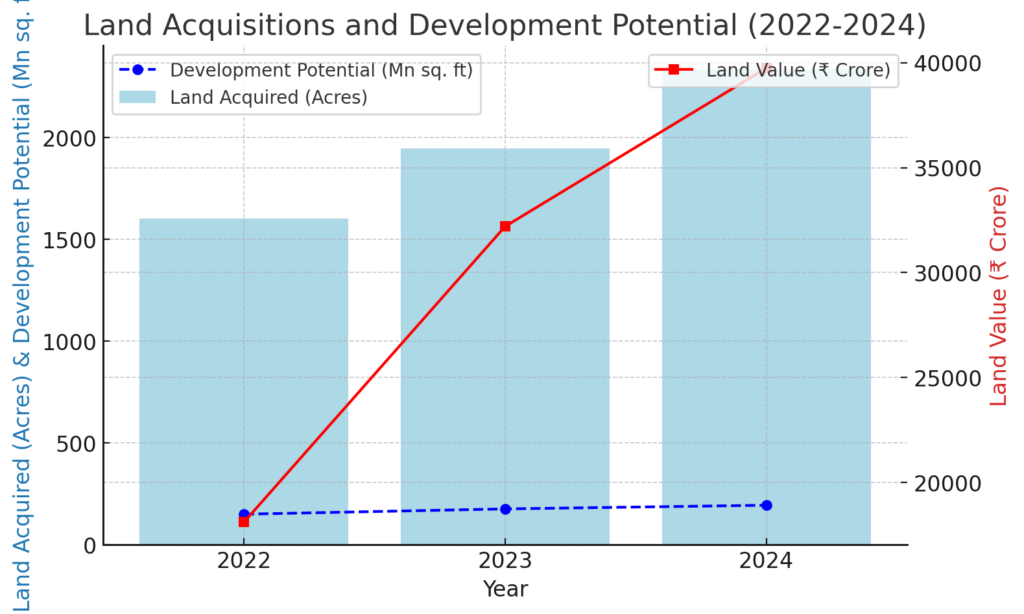

The year 2024 emerged as a landmark period for India’s real estate sector, with developers acquiring a record 2,335 acres of land across 23 major urban centers. According to JLL’s latest report, these acquisitions, totaling INR 39,742 crore, hold the potential for 194 million square feet of development.

Land Acquisitions and Development Potential

Among the key highlights, Tier I cities maintained dominance, securing 72% of the total land acquired. However, Tier II and III cities made significant inroads, capturing 28% of the share, equivalent to 662 acres. Cities like Nagpur, Varanasi, Indore, Vrindavan, and Ludhiana emerged as surprise hotspots, reflecting a strategic shift towards diversified urban development.

Regional Highlights

The Mumbai Metropolitan Region (MMR) led land acquisitions, with 407 acres transacted through 19 deals—up 41% from 2023. Meanwhile, the National Capital Region (NCR) recorded the highest number of transactions, with 36 deals, particularly in Gurugram (21 deals) and Noida (14 deals).

Surge in Residential Development

Residential projects dominated the landscape, comprising 81% of all acquired land, translating to 158 million square feet of potential housing space. Factors such as the Reserve Bank of India’s policy rate cut and fiscal support for the middle class fueled housing demand, prompting developers to bolster supply. Other asset classes, including office, retail, and industrial real estate, saw relatively lower interest.

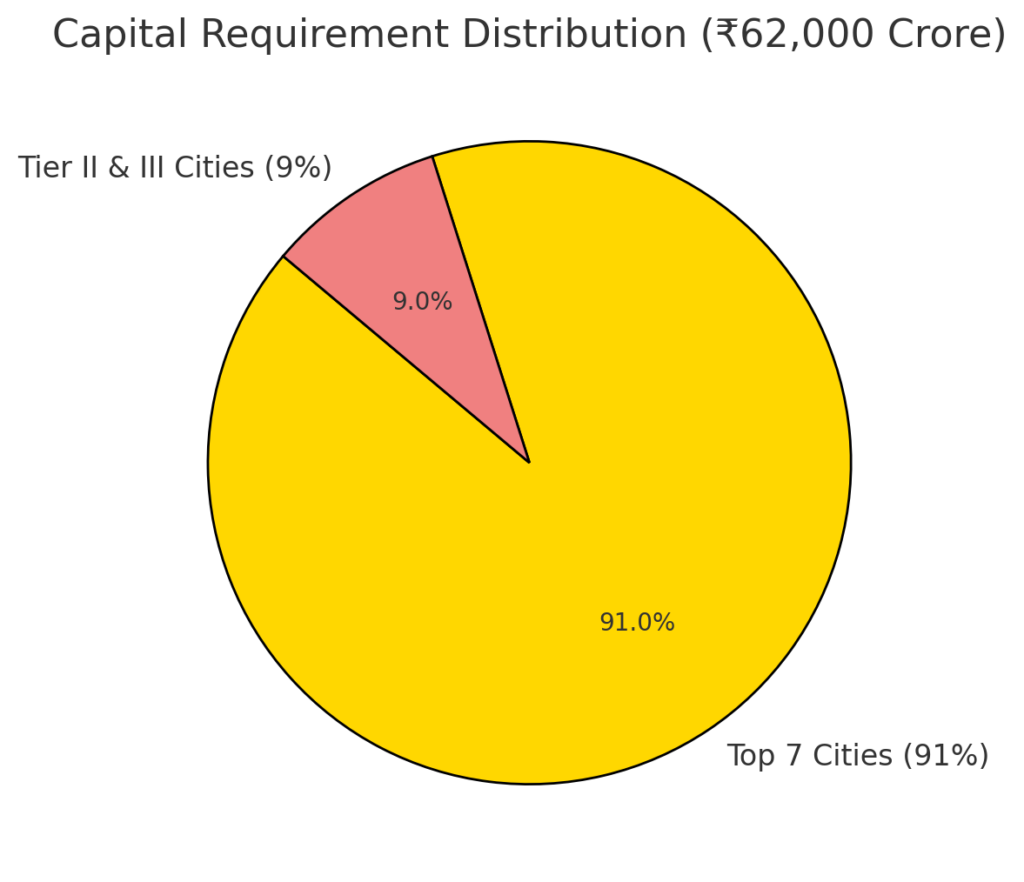

Capital Investment and Financing Trends

Developing these new land acquisitions is expected to require an investment exceeding INR 62,000 crore. The top seven cities—Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata, MMR, and Pune—will account for 91% of the projected capital needs. With traditional financing constraints in place, alternative investment funds (AIFs) and private credit are poised to play a crucial role in meeting funding requirements.

Future Growth Trajectory

JLL’s findings indicate that real estate development is shifting towards a dual strategy—aggressive expansion in top cities alongside steady growth in Tier II and III markets. This approach is expected to create a more balanced and sustainable development pipeline across India’s urban landscape.

SFI Analysis:

The record-breaking land acquisitions of 2024 signify a paradigm shift in India’s real estate sector. While major metros continue to attract investments, the increasing interest in Tier II and III cities underscores a broader market expansion. This shift is driven by urbanization trends, infrastructure development, and rising demand for housing beyond traditional hubs. The surge in residential projects aligns with India’s growing middle class and favorable policy interventions. However, challenges such as rising construction costs and financing constraints remain pertinent. Alternative investment mechanisms, including AIFs and private credit, will be instrumental in sustaining this growth. Moreover, with developers focusing on long-term land banking strategies, India’s real estate sector appears poised for continued expansion, fostering economic growth and urban transformation.

Also Read: Amazon real estate