- Despite repo rate hikes, the avg. cost of debt for top listed players is at its lowest since the pandemic

- Net debt of top eight listed realty players down to INR 208 Bn in Q2 FY23 – lower than pre-pandemic levels

- Listed players sales share up from 16% in FY20 to 23% in FY21

- From 37 Mn sq ft in FY20, top listed players saw sales rise to 41 Mn sq ft in FY21 & further to 57 Mn sq ft in FY22

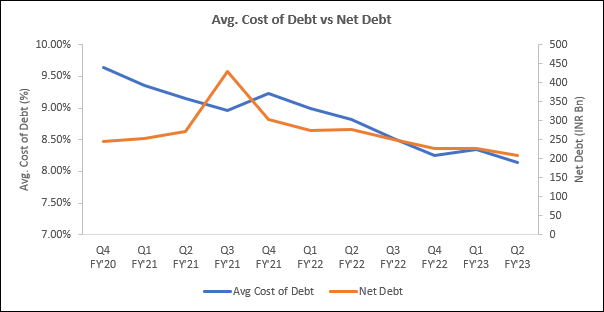

Despite the back-to-back repo rate hikes in 2022, the average cost of debt for the top eight listed realty players is at its lowest since the pandemic. Analysing the financial data of the top listed players reveals that with the rise in sales revenue, their average cost of debt has reduced from 9.64% in Q4 FY20 to approx. 8.14% in Q2 FY23.

The net debt of these developers is down to INR 208 Bn by end Q2 FY23 – lower than the pre-pandemic levels. It was INR 245 Bn by Q4 FY20 and had risen significantly to INR 429 Bn by the end of Q3 FY21.

While funds availability is a challenge for many smaller real estate developers, the larger players – particularly listed players – can raise funds at competitive rates thanks to good track records, high market acceptance and brand trust, and demonstrated financial discipline.

RERA implementation and the IL&FS fiasco had coupled with the economic downturn to create a funding crunch in the real estate sector from 2016-19. Investors were uncertain about the future of the Indian real estate sector and became extremely prudent while evaluating investment options.

“The slew of measures by the RBI and government to increase liquidity during the pandemic helped developers to tide over the difficult times,” says Anuj Puri, Chairman – ANAROCK Group. “These included a reduction in repo rate, loan restructuring, stamp duty cuts, and a relief package to boost the economy. Housing sales gathered momentum on the back of record low home loan rates and stamp duty reductions in some states.”

“This momentum majorly targeted projects by the top listed players, who sold 37 Mn sq ft in FY20, 41 Mn sq ft in FY21, and 57 Mn sq ft in FY22,” says Puri. “Not surprisingly, this ensured that these players could access funds at cheaper rates, significantly improving their liquidity and capital structure.”

Stars aligned for listed developers

The listed players performed well during the pandemic, with their sales share rising from 16% in FY20 to 23% in FY21. This was instrumental in reducing their debt. The net debt of the top eight listed realty players stood at INR 245 Bn as of Q4 FY20, increased significantly to INR 429 Bn at the end of Q3 FY21 due to the pandemic, and then reduced gradually to INR 208 Bn in Q2 FY23 – which is lower than it was before the pandemic.

The average cost of debt also reduced for the listed players as they could negotiate their terms due to their limited funding requirements. The average cost of debt increased slightly during Q4 FY21 as net debt peaked in Q3 FY21, and the requirement of funds briefly rose.

Avg. cost of debt and net debt is at the end of the quarter; avg. cost of debt and net debt data is for the top eight listed players Source: Company Financials, Compiled by ANAROCK Research

With the rise in sales revenue, the cost of debt for the financially strong listed developers reduced markedly – from 9.64% in Q4 FY20 to 8.14% in Q2 FY23. Interestingly, these players witnessed a reduction of 150 bps in the past ten quarters despite a repo rate hike of 150 bps. The gap between the average cost of debt and the repo rate narrowed during the pandemic.

This is attributed to the strong financials and reduced funding requirement by the listed developers, who were able to raise new loans at competitive rates and refinancing their existing loans at lower rates.

Source: RBI, Company Financials, Compiled by ANAROCK Research

Now, on the back of these players’ overall financial strength and robust sales, the average cost of debt has reached its lowest point since the pandemic. As the requirement for funds increases over time, the demand for capital also rises with it, leading to increased cost of debt. If the repo rate keeps increasing at the current pace, it may create upward pressure on the cost of debt.

Also Read: Real Estate’s Budget Expectations – 2023-24