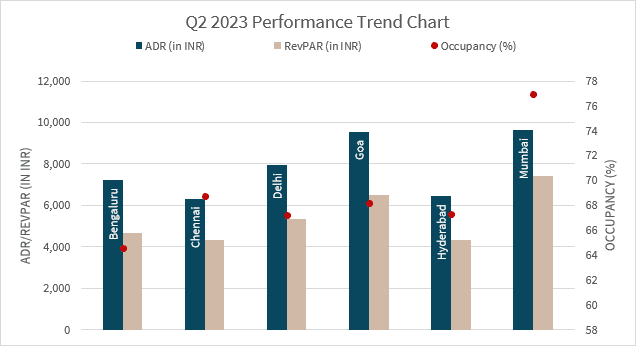

- Chennai witnessed the highest growth in Revenue Per Available Room (RevPAR) in April to June (Q2 2023) at 31.4% over Q2 2022

- Q2 2023 witnessed the opening of 51 new hotels comprising 2,959 keys of which more than 90% were located in Tier II and Tier III cities

- 16 hotels signed in Q2 2023 were conversions of other hotels, which constituted 23% of the inventory signed

The Indian hospitality sector continued to witness Year-on-Year (Y-o-Y) growth in performance in Q2 2023, primarily driven by the significant rise in Average Daily Rate (ADR) of 16.4% over Q2 2022 resulting in a RevPAR growth of 15.4%. The second quarter recorded a dip in occupancy levels due to the onset of the summer vacations that led to a subsequent decrease in corporate travel. Furthermore, the sector witnessed a 16.6% q-o-q decline in RevPAR in Q2 2023, as compared to Q1 2023, according to JLL’s Hotel Momentum India (HMI) Q2, 2023.

Apart from Bengaluru’s marginal drop in occupancy levels amidst summer vacations, the rest of the markets continue to display significant growth in ADR and RevPAR figures. Whilst occupancy levels remain fairly the same in Q2 2023 as compared to Q2 2022, ADR levels have picked up, subsequently pulling up the RevPAR levels across all the 6 major markets.

The following quarter is expected to gain favorably from resurging corporate travel, festivals and other corporate and social MICE. The upcoming G20 events in multiple cities throughout India will boost the hospitality sector, spurring demand for immediate requirements while building the foundation for future growth.

69 hotels comprising 7,010keys were signed in Q2 2023. There were 16 hotels signed that were conversions of other hotels. Conversions constituted 23% of the inventory signed in Q2 2023. Hotel brands continue to be optimistic towards the Indian hotel market not only in the mid-market space but also in the luxury space with the signing of the first Radisson Collection and Waldorf Astoria hotels in Hyderabad and Jaipur respectively.

All six key markets witnessed strong growth in RevPAR levels in Q2 2023 as compared to Q2 2022, due to the continuing contribution of MICE, social events, leisure travel, etc. Chennai emerged as the RevPAR growth leader in Q2 2023 registering a growth of 31.4% over Q2 2022, followed by Delhi and Hyderabad with y-o-y growth of 25.8% and 24.6% respectively.

“Whilst the hotels and hospitality market witnessed a slight dip in corporate room night demand in Q2 2023 amidst summer holidays, the sector continued to display strong growth in ADR levels in Q2 2023 over Q2 2022. The performance of the sector in the coming quarters looks promising on the back of resurgence of domestic corporate demand, MICE, weddings, and other social events. As the tourism and connectivity infrastructure continues to improve, the country is expected to host multiple international events in the coming future. India’s G20 presidency, which has provided a fillip to the performance of the hospitality sector through the year, will draw its curtains in September. However, the sustainable sources of demand such as MICE, social events, and leisure will continue to drive the sector in the months to come”, said Jaideep Dang, Managing Director, Hotels and Hospitality Group, JLL India.

Also Read: Hospitality sector witnesses Growth